I have a confession to make: there is something that most people consider an American classic that, every time I see it, sets my teeth on edge. Where others find heartwarming inspiration, a mere glimpse of it provokes an intense dislike on my part that I freely admit probably borders on the irrational. So here is my confession: I truly loath the classic holiday movie It’s A Wonderful Life.

What? But Pining, don’t you know that It's a Wonderful Life is one of the most critically acclaimed films ever made? Don’t you care that it was nominated for five Oscars and has been recognized by the American Film Institute as one of the best American films of all time, placing number 11 on its initial 1998 greatest movie list? Don’t you care that the film ranks number one on the Film Institutes’ list of the most inspirational American films of all time?

Sorry, but no. I don’t care about any of these things. I view this film as the single greatest piece of propaganda for fractional reserve bank fraud ever created. It irritates me that this sappy, gauzy schlock has become the mental touchstone for generations of people whenever they think about banking or the concept of a bank run. Most of all, I deeply resent the cultural 'cover' that this film has provided for a predatory and largely parasitic industry through the fact that it has successfully implanted into the American consciousness the pernicious fiction that banks, at their core, are essentially “just all of us working together and supporting each other” by sharing and lending the value we earn. In explaining why his and other behemoth financial firms should be bailed out by taxpayers in the wake of their greed-fueled mortgage fraud and derivative implosion, Lloyd Blankfein could never have argued with a straight face “We are doing God’s work” without having the mental battle-space prepared for him well ahead of time by the generations of brainwashing done by It’s a Wonderful Life. What an interesting Christmas miracle it would have been if George Bailey had told the truth about the bankstering classes:

So get that propagandistic “holiday classic” crapola out of your heads, because we are going to talk about bank runs.

Everyone knows that a bank run is when people start to question the solvency of a bank, and they all try to get their money out at once. Because the bank has loaned out more money than they have on hand in deposits, this means they cannot pay everyone(and usually cannot pay even 1 customer in 20) so when the public begins to question the solvency of the firm there is a “run” on the bank as depositors all rush in to try to get their money out before the bank goes belly-up.

This is more or less accurate, but I would point out one thing- what people are panicked about isn’t quite that they may lose their money. At the core of it all, what they are really terrified of is that they might lose the value they have stored in the bank, in the form of money. A carpenter in Loveland, Colorado in February of 1930 wasn’t sprinting off from his job site upon hearing a rumor to try and withdraw the $293 he had on deposit with the local Savings and Loan because he was worried about the actual dollars. What he was terrified of losing was the thousands of hours of his labor, all of his diligent scrimping and saving, and the (to him) precious value of his earned productivity that those 293 dollars represented. He stored his hard-earned value in dollars, then stored those dollars in a bank… and that underlying value those dollars represented was what he was so panicked to preserve.

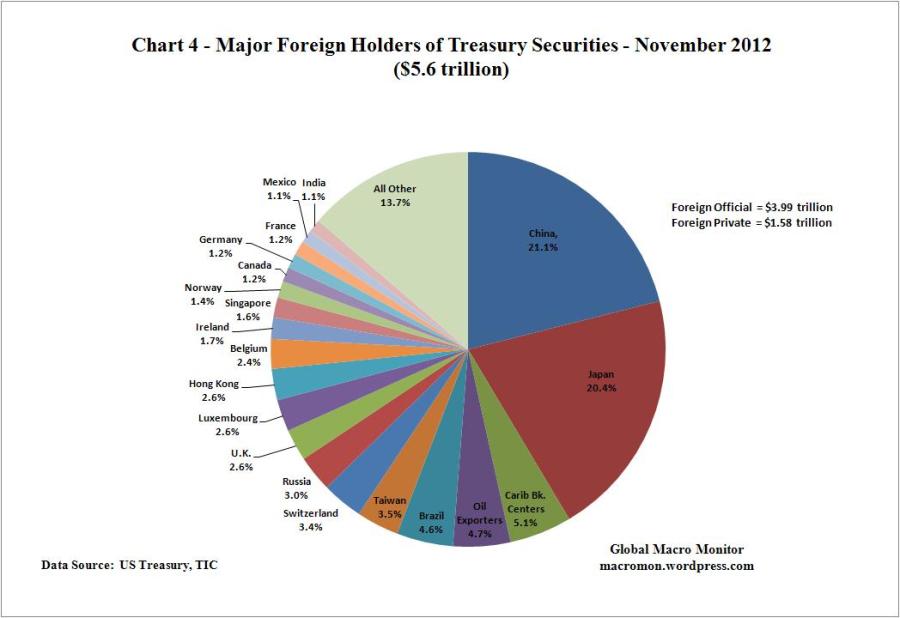

Much like our carpenter and his worries about his local bank, at this moment in time China has 1.2 trillion dollars of stored value, on-deposit with “The Bank of the Dollar” in the form of Treasury bonds. Japan also 1.1 trillion of their hard-earned wealth on deposit in the same bank. The rest of the world has an additional 3.3 trillion combined on deposit with “The Bank of the Dollar”, as the total US Treasury debt outstanding that is held by foreign entities is a whopping 5.6 trillion dollars.

I hate to break the news to you, but there is a run on this bank going on right now. Oh, it's still quiet and there is nothing approaching panic just yet, but make no mistake- these countries are just as worried as our fictional carpenter about getting their stored value out of that bank before everyone else tries to do the same thing. You see, the board of directors of the “Bank of the Dollar” (already on thin-ice amongst their depositors for repeatedly issuing themselves I.O.U. withdrawals and spending them at an alarming rate) just raised the “debt-ceiling” level for this practice that they had set in place to reassure their depositors. In fact, since 1960 they have raised, extended, or changed the definition of this limit 79 times, understandably calling into question their very comprehension of the word “limit”. Not only that, but they now appear to have just done away with the concept entirely, recently granting the CEO permission to withdraw literally un-limited amounts, in perpetuity.

The first sign of an incipient run on the “Bank of the Dollar” is that the major customers are no longer depositing their hard-earned value in this bank. They have ceased making the normal deposits that buying Treasuries represents, which tells us that they are already nervous, and are unwilling to put more of their hard-earned value at risk in this bank:

Image cannot be displayed

Indeed, the quiet selling of this chart can be compared to the townsfolk stealthily making their way into the bank, attempting to appear nonchalant while they withdraw small amounts that will not draw attention and thus not panic the other customers. At some point, everyone will look around at everyone else, their eyes will narrow, and somebody will make a mad-dash for the teller's window and demand all their cash, instantly spooking everyone else into doing the same. The result will be, predictably, chaos.

At that point, woe be to him who still has his value stored at the Bank of the Dollar when the customers bolt and break for the tellers window. There will be no heartwarming ending when the townsfolk rally around poor George Bailey, saving him from his fractional reserve shenanigans and poor risk management.

There is one other thing I would like to mention about bank runs, and it provides a peculiar connection to the Federal Reserve. In the early 20th-century, there was a banker in Utah named Marriner Eccles. He was the son of a polygamist lumber magnate named David Eccles, who made his fortune illegally cutting timber on huge swaths of western Federal lands, then bribing local officials to produce the proper signatures and paperwork when questions arose. When this failed, he bribed Federal Judges to throw trials. Anyway, son Marriner used his inherited wealth to purchase numerous banks in Colorado and Utah, and in the aftermath of the great stock market crash of 1929, he built his reputation based on his methods of dealing with bank runs. When Marriner sniffed a run coming, he would arrange for large bundles of cash (in small denominations, so there were many bundles) to be delivered and he would deliberately truck this cash straight through the waiting crowd in the lobby just prior to the bank opening. Marriner would then stand in the lobby making a great show, grandly announcing that the bank had plentiful reserves of cash, and that anyone who wanted their money would get their money even if he had to keep the bank open late into the night. On the second day, he would do the same thing but would instruct his tellers to count out each customer’s cash as slowly as possible, dragging out each transaction and minimizing the number of customers who could withdraw their money. On the third day, he would arrange for “plants” to stand in the Deposit line, so that when customers entered the bank they would see people cued-up to deposit, not withdraw, cash.

Please note that each and every one of these techniques was a deliberate deception- a psychological ploy to fool people into thinking that the bank really did have all their money, which of course it did not. These tricks were nothing more than a ploy to hide the dismaying truth that the bank had lent out their money long ago, but the grand show would fool people into thinking that the carefully saved value of a lifetime of hard work was far less at-risk than it actually was. Marriner Eccles gained a national reputation during this time, and in a few years would be named Chairman of the Federal Reserve.

Today, the people who go to work at the Federal Reserve Headquarters in Washington D.C walk through the doors of the Marriner Eccles building, a grand structure named for a man whose reputation was built on tricking and deceiving people about the genuine risk of losing their hard-earned life savings... and the greater the risk, the more elaborate was his deception to hide it. Somehow fitting, don’t you think?

When the run on the “Bank of the Dollar” begins in earnest, I expect that the people in this building will fully live-up to its namesake’s legacy, and that no deception will be beyond the pale to protect the interests of their firm. Indeed, one could argue that, from interventions in the Treasury and currency markets to the suppression of precious metals prices, they are already heavily engaged in the practices that made Marriner Eccles reputation. I seriously doubt, however, that the Chinese or others will be fooled by their parlor tricks.

You shouldn’t be either.

Keep stacking.

--------------------------------------------------------------------------------------------------------

* A quiet thank you and respectful farewell to the anonymous and utterly brilliant blogger who created the now defunct site Finem Respice. Internet legend has it that this person was the original Marla Singer of the early days of Zero Hedge, and between spinning tunes at RadioZero back in those days, she wrote some of the earliest and best analysis of the true goings-on behind the scenes of the 2008-2009 financial crisis. Whether this is really who this person was or not, the posts at Finem Respice were simply genius and will be missed. The section on Marriner Eccles in this piece was inspired by a post she did that is no longer available online, so because I could not link to her original work, I hope this heartfelt thank you will suffice.